House prices fell in March as the market lost momentum, with rising geopolitical tensions in the Gulf pushing up mortgage rates and creating fresh uncertainty over the outlook for inflation and borrowing costs. While the spring market has started steadily, it remains unclear how long global pressures will persist or how strongly they will feed through into housing market activity.

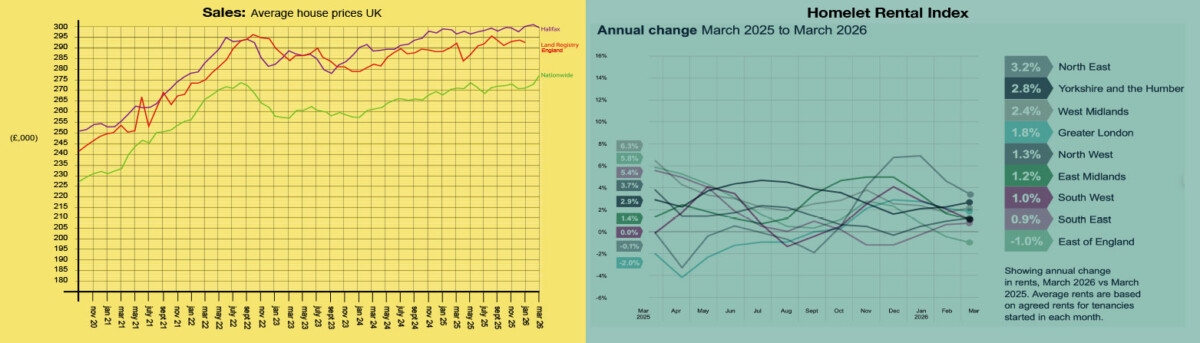

The latest data from Halifax shows that the average UK house price fell by 0.5% in March to £299,677, reversing February’s 0.3% increase. Annual growth also slowed to 0.8%, down from 1.2% the previous month, with early-year momentum beginning to fade.

Amanda Bryden, Head of Mortgages at Halifax, said:

“The recent slowdown in the housing market reflects the wide uncertainty regarding the conflict in the Middle East. Concerns about higher energy prices have pushed up inflation expectations, which in turn led to a rise in mortgage rates, reducing confidence that interest rates will be cut this year and dampening the initial momentum in the market seen at the start of the year.”

Other indicators, though, suggest the market remains resilient beneath the surface. HMRC data shows that UK residential transactions rose by 5.6% in February to 102,410, while mortgage approvals increased by 3.9% to 62,584, although both remain below last year’s levels.

The latest survey data, however, points to softer demand ahead. The latest RICS Residential Market Survey shows new buyer enquiries falling further into negative territory, while agreed sales have also declined, reflecting weaker near-term confidence.

Regional differences remain pronounced. Northern Ireland continues to record the strongest annual house price growth at 8.7%, followed by the North East at 5%, while southern regions are weaker, with prices down 1.9% in the South East and 1.2% in London.

Rightmove, which has the most up-to-date data of all the indices, takes a similar view, with the portal’s property expert Colleen Babcock saying:

“Market activity remains stable so far despite the new global uncertainty over the last few weeks, though it’s too early to tell what may happen later down the line.

That said, uncertainty is never helpful for market activity, and it’s come at a time when confidence and optimism would usually be building as the spring market gets underway.”

Signs, though, are starting to emerge that diplomatic efforts in the Gulf may be gaining traction, with the possibility of renewed talks between the US and Iran and increasing optimism that there could be room for compromise. That could have a major knock-on effect on the outlook and confidence in the housing market.

HOUSE PRICES AND STATISTICS

In a reflection of the current uncertain conditions, the latest indices are more mixed than usual, with Halifax reporting a monthly fall in March, while Nationwide recorded a modest price rebound.

Rightmove: Mar: Avg. price £371,042. Monthly change +0.8%. Annual change -0.2% (asking prices)

Nationwide: Mar: Avg. price £277,186. Monthly change +0.9%. Annual change +2.2%

Halifax: Mar: Avg. price £299,677. Monthly change -0.5%. Annual change +0.8%

Land Registry (England): Jan: Avg. price £293,437. Monthly change -0.2%. Annual change +1.1%

Zoopla: Feb: Avg. price £270,500. Annual change +1.3%

BUY-TO-LET

The rental market is moving into a more balanced phase as demand continues to weaken and supply improves, easing pressure on tenants and slowing rental growth

Zoopla’s latest data shows rents for new lets are now rising at a slower pace, with annual growth at 1.9%, down from 2.8% a year ago. At the same time, demand for rental homes has fallen by 14% year-on-year, while the number of homes available to rent has increased by 11%, giving tenants more choice.

This shift is reducing competition across the market. The number of enquiries per property has fallen to 4.8, the lowest level for six years, while the average time to secure a tenant has risen to around 20 days, giving renters more time to make decisions.

Supply remains constrained, though, from a historic perspective, despite recent improvements. Zoopla says the number of homes available to rent is around 23% below pre-pandemic levels, which means rents are expected to continue rising through 2026, albeit at a more moderate pace of around 2–3%.

The easing in demand is being driven in part by lower migration and more first-time buyers moving out of the rental market, which is helping to free up supply and rebalance conditions after several years of intense competition.

As ever, there are pronounced regional differences, with stronger rental growth in more affordable northern cities such as Liverpool, Newcastle and Glasgow, while the higher-cost markets in the South are seeing much weaker growth or slight declines as affordability pressures limit further increases.