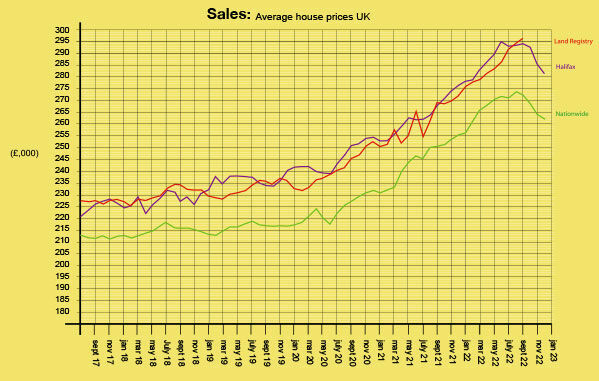

At the start of 2022, with concern mounting over inflation, commentators were expecting modest house price growth of between 3% and 5%. However, with three prime ministers, the war in Ukraine, spiralling energy costs, a new monarch, the cost-of-living crisis and a rising base rate, 2022 defied all expectations.

Driven by the disparity between supply and demand and the ongoing race for space, the housing market began the year briskly and prices rose by 0.3% in January. In February, growth accelerated to 2.3% – the largest monthly increase in 20 years. War, however, was looming and in March, Russia invaded Ukraine and the price of food and energy soared. Despite it all, house prices continued their upward trajectory, rising by another 1.7%. By May, although the base rate had hit 1.0%, house prices had reached a record high of £367,501 (+2.1%), the fourth record-breaking month in a row. It wasn’t until August that there was any kind of fall, but it was only the usual summer slowdown, as many buyers put their purchases on hold while they took their first holidays since the onset of Covid.

As autumn loomed, Boris was ousted, Liz Truss became Prime Minister and her now notorious mini-budget unleashed chaos on the financial markets. The base rate shot up to 2.25% and the average fixed-rate mortgage hit 6.65%. The appointment of Rishi Sunak as Prime Minister soon calmed things down but he has inherited some serious economic challenges – double-digit inflation is generating a wave of strikes, the bank rate has climbed to 3.5% and, although average fixed-rate mortgages have now come down to 5.24%, they are still a long way above the 1.59% of twelve months earlier. And, for the first time in 2022, house prices are reacting as you might expect – falling by 1.1% in November and by 2.1% in December. They still, though, ended the year 5.6% up on 2021. (Figs: Rightmove).

So, after such a tumultuous year, what on earth are the experts predicting for the housing market in 2023? The good news is, most believe inflation and mortgage costs have already peaked and should be coming down this year. However, with real wages falling and mortgage costs still high, especially when compared to the sub 1% rates we were used to, affordability is likely to become increasingly stretched, especially for first-time buyers. As a consequence, most experts are forecasting price falls of between 3% and 10%, with low transaction volumes and an ongoing reversal of the flight from the cities. The falls, however, would only partly undo the substantial house price gains made over the last couple of years.

2022: the facts

Nationwide: Dec 21 to Dec 22: National £262,068 +2.8%. London £528,000 +4.1%

Halifax: Dec 21 to Dec 22: National £281,272 +2.0%. London £541,239 +2.9%

Land registry (3 months in arrears): Oct 21 to Oct 22: National £296,422 +12.6%. London £541,7205 +6.7%

Zoopla: Nov 21 to Nov 22: National £258,100 +8.2%. London £541,720 +6.7%

Rightmove: Dec 21 to Dec 22: National £359,137 +5.6%. London £666,507 +4.6% (asking prices).

The predictions

Please note – where possible, figures from 2022 are from the predicting company’s own indices.

Nationwide

Last year, Nationwide was expecting the market to slow and prices to go up somewhere between 0% and 2%. Although their final figure was close at 2.8%, they had not, like most others, foreseen it would come after a prolonged period of rapid growth. For 2023, they have said there is likely to be a modest decline of around 5%.

Halifax

Halifax didn’t give an exact figure for their prediction last year but were expecting the market to cool. This year, they are factoring in an 8% fall but point out that that would only mean the cost of the average property returning to April 2021 levels.

Zoopla

Zoopla had predicted growth of 3% in 2022, which was some way below their figure of 8.2% (Nov). Their forecast was, however, far closer to the other indices’ figures of between 3% and 5%. For 2023, they have predicted prices will dip by 5%, with smaller falls in the more affordable areas.

Rightmove

Last year Rightmove expected high demand and a shortage of available property to push up prices by 5% nationally and by 3% in the capital. They were very close to their final of +5.6% nationally but were less so with London at 4.6%. Of all the commentators, Rightmove is expecting the softest landing for house prices in 2023, with a drop of just 2% and some wide variation across the UK.

A selection of other predictions

CEBR were somewhat wide of the mark with their expectations of a market slowdown but were closer with their prediction of a 2% rise. This time around, they are expecting house prices to fall by 4.5% by the end of 2023, but with a peak contraction of 6.2% in the third quarter.

EY ITEM Club were rather pessimistic with their prediction that growth would slow markedly in 2022 and that prices would only just remain in positive territory. And they are also some of the biggest pessimists about 2023, forecasting house price falls in double digits.

Capital Economics went for one of the higher predictions in 2022 – a rise of around 5% – but have gone into reverse for 2023 with their rather gloomy prediction of a 12% fall.

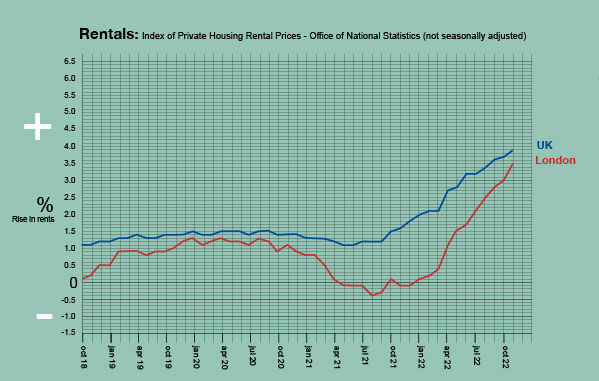

Rental market

Last year, most experts were forecasting unprecedented levels of demand and severe stock shortages for the rental market. And they were right.

From day one, there was a huge imbalance between supply and demand, with demand up by 32%, and supply down by 51% when compared to the previous January and rental properties being snapped up in just 17 days. With many landlords taking advantage of the buoyant sales market to sell off some of their portfolios, the gap between supply and demand just kept on growing. The problem was especially acute in London, where the reversing of the race for space led to some of the UK’s biggest spikes in demand.

And, unlike the sales market, rents just kept on rising through spring, summer, autumn and winter. There were, though, increasing concerns, amidst the cost-of-living crisis, about whether tenants’ finances would be able to cope. As the year wore on, landlords’ costs also began to rise, especially for mortgages and energy, placing yet more upward pressure on rents. With the steepest rises to be found in newly listed properties, many tenants elected to stay put. At the same time, locked out of the sales market by increasing mortgage costs, aspiring first-time buyers had no choice but to remain in the rental sector.

By the end of the year, the UK’s average rent had climbed to £1,174, an increase of 10.8%. In London, rents rose even higher – 14.6% – breaking through the £2k barrier for the first time at £2,007pcm. The biggest rise of all, though, was to be found in London’s Hackney and Newham, where rents shot up by a staggering 22.8% during 2022.

Most commentators are expecting a very similar story in 2023, with a recent survey by lender, Aldermore, finding landlords planning on raising rents by another 10%. 64% of them are also worried tenants may not be able to afford the rise, and that that could lead to increasing arrears.

Andy Halstead, HomeLet and Let Alliance CEO, says:

“Our prediction for 2023 is that rental prices will likely continue to rise, despite spiralling costs for tenants in other areas of their lives. Tenants struggling to pay their rent is sadly likely to become a recurring theme across the country, and in turn, this could lead to some landlords vacating an already struggling market. This will likely result in a continued shortage of rental properties to meet demand.”