The first housing data of 2023 is starting to emerge, giving us an early indication of the market’s direction of travel. Rightmove’s figures show there was a pronounced post-Christmas bounce in January. According to them, asking prices rose by 0.9% and buyer activity was up by 55% from the previous month. In contrast, Nationwide’s index shows prices fell by 0.6% and annual growth dropped to 1.1%.

So, why the contradiction and what does it mean for the housing market in 2023?

When looking at housing data, it is important to bear in mind that not all indices are compiled in the same way. Rightmove’s figures, for example, are based on current asking prices and are therefore affected by market sentiment. Nationwide’s and Halifax’s are based on sold prices, so they are more accurate but can sometimes run a month or so behind. It means, if you want the most up-to-date figures, Rightmove’s index is the most useful, although the bounce they are reporting in January is a little misleading. A bounce is a common occurrence at this time of year and, even though demand was 4% above typical pre-pandemic levels (January 2019), it was a third below the more frenetic activity of the same period in 2022.

What it does show is that the market appears to be overcoming much of the hysteria engendered by Liz Truss’ mini-budget and is returning to pre-pandemic levels for both prices and demand. There are several factors behind the better-than-expected data – despite increases in the base rate, mortgage rates are continuing to come down (the best five-year fixed rates have now fallen below 4.0%), inflation is likely to have peaked and both consumer confidence and the economic outlook are improving. In addition, prices are being supported by ongoing shortages in supply caused by the failure to build sufficient new homes.

Tim Bannister Rightmove’s Director of Property Science says:

“Given that the pause for Christmas came unexpectedly early last year, it was important to see whether buyers and sellers would pick up their plans again at the beginning of this year or wait to see what the first few months might bring. The numbers certainly suggest that activity has bounced back after Christmas and agents will now be busy trying to match the likely revised expectations of buyers and sellers as we move towards the important spring season.”

Most commentators also point out, however, that the house price rises of the last couple of years, the cost-of-living crisis and higher mortgage payments mean affordability is now seriously stretched, which will keep a firm lid on prices. Stretched affordability, and commuter costs, have also resulted in a growing demand for flats rather than houses, especially in more urban areas. According to housing portal, Zoopla, searches for 1 and 2-bed flats have gone up from 22% of all searches to 27%. In London, the numbers are even higher, with 1 and 2-bed flats accounting for 49%, up from 42% in 2022. And, in a process agents are attributing to ‘buyer remorse’ over the flight to the country, a high proportion of those buyers are coming from rural areas.

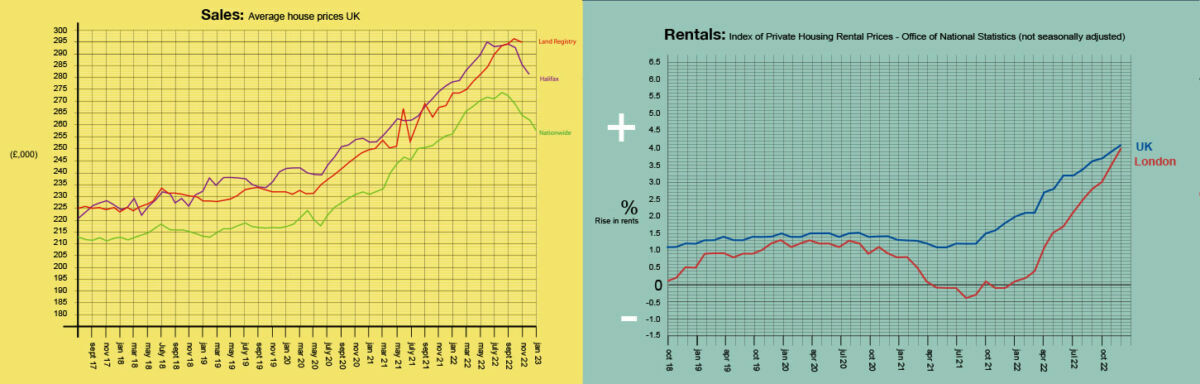

HOUSE PRICES AND STATISTICS

Of the three most up-to-date indices, only Nationwide’s fell last month. Rightmove’s and Halifax’s show the market stabilising after falls at the back end of 2022.

Nationwide: Jan: Avge. price £258,297. Monthly change -0.6%. Annual change +1.1%

Halifax: Jan. Avge. price £281,684. Monthly change 0.0%. Annual change +1.9%

Land Registry: Nov: Avge. price £294,940. Monthly change -0.3%. Annual change +10.3%

Zoopla: Dec: Avge. price £259,100. Monthly change +0.1%. Annual change +8.1%

Rightmove: Jan: Avge. price £362,438. Monthly change +0.9%. Annual change +6.3% (asking prices on Rightmove)

BUY-TO-LET

Affordability is also a serious issue in the rental market, with ever-rising rents pushing tenants’ finances to their limits. According to a recent survey, tenants are now spending an average of 24% of their income on rent. In London, it is as much as a third of their incomes. As a result, despite the continuing gap between supply and demand, rents have fallen for the second month in a row. In December, the average was down by 0.2% to £1,172pcm (figs: Homelet). Rents are expected to resume their rise over the coming months, but not at the same frantic pace as before.

Andy Halstead, HomeLet and Let Alliance CEO, warns:

“The cost-of-living crisis shows few signs of abating anytime soon, with tenants facing rising costs across all areas of their lives. The increasing pressure on tenants looks likely to have a knock-on effect – tenants facing difficulties paying rent could see landlords choosing to exit the market altogether, leading to a spiral that exacerbates the shortage of rental properties and further drives prices upwards.”

In the past, people have been quick to blame ‘greedy landlords’ for any rises, but there is a growing realisation that the blame lies, instead, at the government’s door. Unlike other businesses, landlords are unable to offset their finance costs against their revenues. With mortgage costs rising, many are being forced to either increase rents to cover their costs or are selling up. The press is, at last, highlighting the issue, putting some much-needed pressure on the government to take action. But will they dare give a tax break to landlords, even if it is in the best interest of tenants?